The “Unlimited Subscription” Bug & The Sandbox Framework

Introduction: The “Unlimited Subscription” Bug

In the tech world, we know exactly what happens when an API runs without limits. No rate limiting. No monitoring. No governance. Eventually? The server crashes.

Now, let’s talk about a real-world scenario that behaves exactly the same way: ongoing financial support for your grown kids. Many parents don’t realize they’ve accidentally created an “Unlimited Subscription Plan” for their family. There is no defined scope, no boundaries, and no expiration date. Just recurring “support tickets” that require immediate payment:

- Emergency car repairs.

- Rent shortfalls.

- Credit card “bailouts.”

What starts as “short-term help” quietly becomes a permanent installation. This is what I call a Financial Resource Leak. If you don’t implement financial boundaries with adult children, your retirement plan becomes the server that absorbs all the traffic until it fails.

This isn’t about being cold or cutting off your kids. This is about moving from chaos to architecture. It’s about shifting from reactive support to structured systems—moving from “Production Mode” to “Sandbox Mode.”

The Strategic Goal: Implementing Financial Boundaries with Adult Children

Let’s clarify something immediately: we are not talking about abandoning your child. We are talking about redesigning the system. Right now, many parents operate in Production Support Mode:

- You own the bug: When they overspend, it’s your problem.

- You fix the issue: You spend your time figuring out their finances.

- You pay for the patch: Your savings cover their mistakes.

- You absorb the consequences: Your retirement is delayed.

That model might be sustainable when they are 15, but it is a system failure when they are 35. The goal of financial boundaries with adult children is to move to a Financial Sandbox Environment. In software, a sandbox is limited, controlled, safe, and isolated from the core system.

When applied to parenting, a sandbox means:

- They are allowed to make financial decisions.

- They are allowed to make mistakes (bugs).

- They operate within defined limits (rate limiting).

- Your core retirement assets remain protected.

You are no longer the Chief Financial Officer (CFO) of their life. You are now a Senior Advisor.

-

Identify the “Invisible Resource Leaks”

Before you can fix a memory leak in a program, you must detect it. The same applies to your bank account. Most parents underestimate how much they are spending on adult children because the expenses are scattered. They feel small, temporary, and helpful, but collectively, they are draining your long-term wealth.

The Audit: Trace Every Financial API Call

Start with a full audit of your “Financial API.” Look at your bank statements and ask:

- Are you still paying their Netflix or Spotify?

- Are you covering their car insurance or phone plan?

- Are you paying for health premiums or rent supplements?

- Are you sending random “quick transfers” via apps for groceries or gas?

These are tiny API calls. Each one seems harmless, but together they create continuous background processing that slows down your own financial growth.

The Calculation: Let’s say you’re paying:

- $120 for their phone

- $180 for their insurance

- $450 for miscellaneous “help” Total: $750/month.

Over a year, that is $9,000. Over 10 years, it is $90,000 (without accounting for compound interest). That is not just “helping”; that is a silent pension withdrawal. One of the most powerful first steps in building financial boundaries with adult children is visibility. You cannot manage what you do not measure.

The Action: Create a “Statement of Support”

Write it down. Create a document titled: Statement of Financial Support. List every recurring payment, emergency transfer, and co-signed liability. Put the annual total at the bottom. Seeing the full number changes the conversation from emotion to data. Awareness is the first firewall.

-

Implementing the “Sandbox” Protocol

In tech, a sandbox isolates code execution from the main production system. If the code breaks, the core stays safe. Now let’s apply that to money.

The Strategy: Replace Reactive Bailouts with a Fixed Allocation

Right now, your support is likely reactive. Your child calls, an emotion spikes, and money transfers. Instead, move to a proactive structure. Offer a fixed monthly support allocation—if you choose to provide one. Think of it as a Monthly Consulting Retainer. It is not unlimited, not reactive, and not negotiable mid-cycle.

Example: “Starting next month, I can provide $400 monthly for 6 months while you transition your budget.”

The Rule: Once Funds Are Gone, Access Is Denied

In programming terms, when sandbox funds hit zero, the system must return a 403 Forbidden error.

- No emotional overrides.

- No guilt-based patches.

- No emergency exceptions unless they meet your pre-defined “Tier 1” criteria.

Scarcity teaches prioritization. When there are limits, spending becomes intentional and accountability increases. Financial boundaries with adult children don’t harm growth; they create the environment where growth is finally required.

Why This Protects Your Wealth Architecture

You worked decades building your financial architecture. Your retirement accounts, your home equity, and your emergency funds were not built to be an open API endpoint for others. When you fail to implement financial boundaries with adult children, you expose your core system to uncontrolled access, which always results in system instability.

The sandbox protects your retirement cash flow, your healthcare buffer, and your peace of mind. Surprisingly, it also improves your relationship because resentment decreases when structure increases.

The Documentation Layer & Emergency Tiering

-

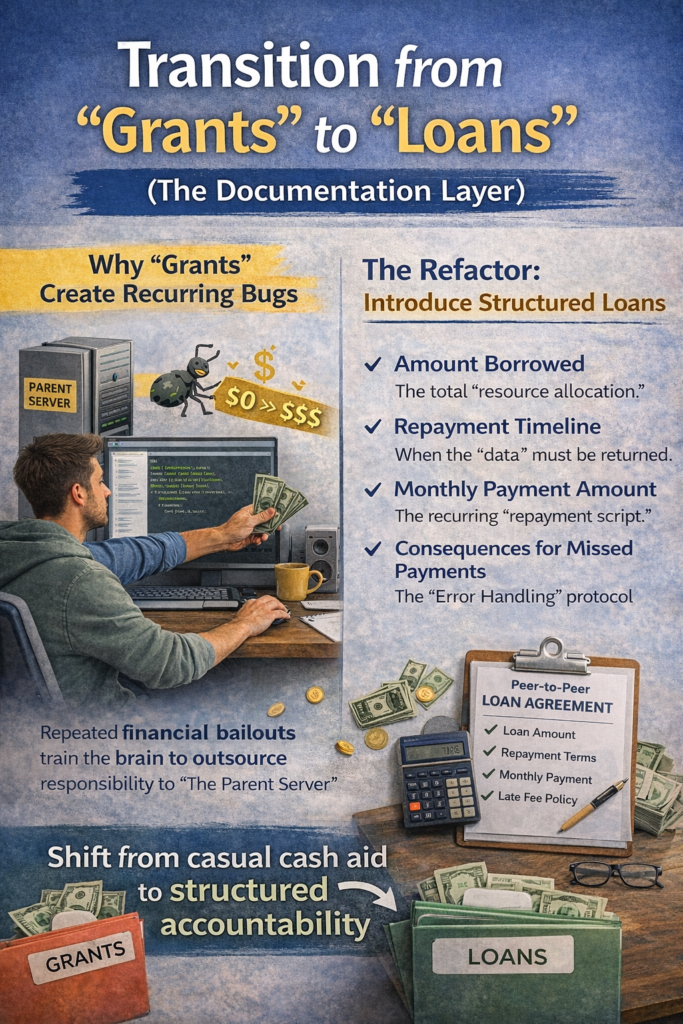

Transition from “Grants” to “Loans” (The Documentation Layer)

When money is treated as a gift, something subtle but dangerous happens: accountability disappears. In software terms, you’re patching the symptom (lack of cash) without fixing the bug (poor financial habits). If you truly want to implement financial boundaries with adult children, you must add a documentation layer. Documentation changes the psychology of the transaction.

Why “Grants” Create Recurring Bugs

When a child overspends and you immediately provide a grant to cover it, you are running a recurring script. Grants remove the friction that is necessary for optimization. If there is no consequence, there is no reason for them to refactor their budget. Repeated financial bailouts actually train the brain to outsource responsibility to “The Parent Server.”

The Refactor: Introduce Structured Loans

For larger requests—security deposits, car repairs, or tuition gaps—shift from grants to structured loans. This doesn’t mean you’re being cold; it means you’re formalizing the relationship and showing them that you respect them as adults.

A simple Peer-to-Peer Loan Agreement should include:

- Amount borrowed: The total “resource allocation.”

- Repayment timeline: When the “data” must be returned.

- Monthly payment amount: The recurring “repayment script.”

- Consequences for missed payments: The “Error Handling” protocol.

The Psychological Shift

When money is documented, spending decisions suddenly become thoughtful. Risk-taking decreases and entitlement reduces. Even if you later choose to “forgive” a portion of the loan for a birthday or holiday, the behavioral shift of being accountable to a contract has already occurred. You are no longer the CFO; you are a lender with terms. This subtle difference is a cornerstone of financial boundaries with adult children.

-

The “Emergency Tier” Definition

Now we need to talk about one of the most emotionally charged areas: “Emergencies.” Without a clear definition, every minor inconvenience becomes a “Critical System Failure.” And when everything is urgent, your boundaries will collapse.

Defining Tier 1: Critical Emergencies

These are true system failures that justify a manual override of your boundaries. Examples include:

- Unforeseen medical bills.

- Personal safety threats or domestic instability.

- Legal crises that affect basic survival.

In these cases, support is reasonable, but it should still be structured. Emergency support does not mean an unlimited ongoing subsidy; it means stabilizing the system until it can run on its own again.

Defining Tier 2: Non-Critical Requests

This is where the majority of “financial leaks” happen. Examples include:

- Late fees from poor planning.

- Travel expenses for weddings or vacations.

- Credit card debt from lifestyle overspending.

- “I didn’t budget for my car registration.”

These are not system failures; they are Planning Errors. If you want to build real financial boundaries with adult children, you must allow planning errors to produce natural consequences. A late fee is the “Log File” that teaches budgeting. When you eliminate the lag between a poor choice and its consequence, you eliminate the possibility of learning.

The Script for a “Tier 2” Rejection

“I care about you, and I believe you’re capable of solving this. I’m not going to step in for this situation, but I’m happy to sit down and help you create a plan to avoid this next month.”

You are withholding the money, but offering the wisdom. That is strategic compassion.

-

Decommissioning the “Safety Net” Gradually

In tech, you don’t shut down a mission-critical legacy system overnight unless you want a total crash. You phase it out. If you are currently providing significant monthly support, we will implement the Step-Down Method.

The Step-Down Strategy

Let’s say you are currently providing $500/month in rent support. You don’t go to $0 tomorrow. You set an “End-of-Life” (EOL) schedule for the support:

- Month 1: $400

- Month 2: $300

- Month 3: $200

- Month 4: $100

- Month 5: $0 (System Retired)

Communicate this timeline in advance and put it in writing. This gives your adult child time to increase their income, find a roommate, or reduce their “Operating Expenses.” It also gives you time to emotionally detach from the role of “Provider.”

Why Gradual Withdrawal Works

Abrupt shutdowns create panic and resentment. Gradual reduction creates Adaptation. Their financial awareness increases as the safety net shrinks. Most importantly, your retirement fund stops “bleeding” out. Financial boundaries with adult children are not about shock therapy; they are about intentional, professional transitions.

The Hidden Risk: Enabling Delayed Adulthood

There is a growing pattern of “Extended Adolescence” caused by parental over-support. Adulthood is built through the friction of managing bills and solving problems independently. When you eliminate the discomfort of adult life, you accidentally eliminate the maturity that comes with it. Protection, when excessive, becomes a limitation on their potential.

Communication Protocols & Emotional Debugging

-

Protecting Your Marriage Through Financial Boundaries with Adult Children

Setting financial boundaries with adult children is rarely just about the money; it is an identity conversation. You are shifting your role from “Provider” to “Advisor,” and they are losing a safety net. If you communicate poorly, it feels like rejection. If you communicate clearly, it builds respect.

The Timing: Don’t Announce Boundaries During a Crisis

The biggest mistake is introducing new rules in the middle of an emergency. When your child calls because they are stressed and short on cash, saying “I’m done helping” feels like an attack.

- The Fix: Choose neutral timing. Schedule a “System Sync” conversation when things are calm.

- The Script: “I’ve been reviewing my long-term financial plans for retirement, and I want to talk about how we handle support moving forward to ensure we are both stable.”

The Tone: Calm, Clear, and Non-Defensive

Expect pushback. They may say, “You have the money, why are you being selfish?” If you defend yourself emotionally, the discussion spirals into a “System Loop.”

- The Response: “I love you and I believe in your ability to manage this. Managing my finances responsibly is how I ensure I won’t have to depend on you later in life.”

-

Managing Guilt When Setting Financial Boundaries with Adult Children

When you implement financial boundaries with adult children, you are interrupting a dependency cycle. Their “Operating System” is used to your support, and change feels threatening.

Understanding the Dependency Cycle

If support has been consistent for years, entitlement often forms unintentionally. When you change the system, their nervous system reacts with “Emotional Turbulence.” This might include:

- The Guilt Trip: “Other parents help their kids, don’t you care?”

- The Accusation: “You’re abandoning me when I need you most.”

- The Withdrawal: Going silent to punish you for the boundary.

The “Broken Record” Technique

Manipulation requires your active participation. If you don’t engage in the argument, the script loses power. Use steady repetition:

- Child: “You’re ruining my life.”

- You: “I understand this feels hard right now. I still believe you can handle it.”

- Child: “Just help one more time!”

- You: “I’m sticking to the step-down plan we agreed on.”

-

Creating a Family Financial Policy

Businesses operate on policies to remove emotional bias from decision-making. Why shouldn’t families? A written Family Financial Policy eliminates confusion and “Legacy Bugs.”

What to Include in Your Policy:

- Monthly Support Limits: The maximum “Bandwidth” available.

- Loan Requirements: The “Documentation Layer” needed for any transfer.

- The “No Co-signing” Rule: A permanent security setting to protect your credit.

- Annual Review: A scheduled “System Audit” to adjust for inflation or changes.

When expectations are written down, every financial interaction becomes procedural rather than personal. Instead of saying “Why won’t you help me?” the conversation becomes “This falls outside our agreed-upon policy.” This subtle shift is a masterclass in financial boundaries with adult children.

-

When to Say “No” with Confidence

There will be moments when the only correct response is a hard No. Confident refusal requires internal alignment. If you doubt yourself, your child will sense the “System Vulnerability” and push harder.

The Internal Checklist Before Refusal:

- Does this request violate my “20-Year Roadmap”?

- Is this a preventable issue caused by poor planning?

- Will helping now delay their “Adulthood Migration”?

- Am I acting out of guilt or wisdom?

If the answer points to a refusal, stand firm. Short-term disappointment in your child often leads to long-term respect for you as a stable leader.

-

Rebuilding Respect After Years of Over-Support

If you’ve already created a dependency, don’t panic. It is never too late to “Refactor” the relationship.

- Step 1: Acknowledge the Pattern. “I realize I’ve been stepping in too often, and I want to adjust our process.”

- Step 2: Implement Structure Gradually. Use the step-down method we discussed in Part 2.

- Step 3: Allow Discomfort. Watching them struggle is the hardest part for any parent, but struggle is the “Compiler” that builds adulthood.

Marital Firewalls & Estate Architecture

-

How Financial Over-Support Impacts Marriage and Retirement Stress

When we talk about financial boundaries with adult children, the conversation usually stays on the parent-child dynamic. But there is another critical system being affected: Your Marriage.

The Silent Marital Strain

In many households, one spouse is the “Enabler” (inclined to give) and the other is the “Architect” (anxious about the long-term cost).

- The Enabler says: “They’re our kids, they need us.”

- The Architect thinks: “We’re draining our pension, who will help us when we’re 80?”

If this tension isn’t resolved, it creates financial anxiety and hidden resentment. You might find yourself hiding bank transfers from your partner just to avoid an argument. This is a “System Breach” of your marriage. Financial boundaries with adult children begin with marital boundaries first.

The Retirement Anxiety Loop

Every dollar redirected to ongoing adult support is a dollar removed from your Compound Growth. Over 15–20 years, consistent “temporary” support can quietly drain six figures from your nest egg. This creates a cycle where your retirement timeline shifts further away, increasing your stress and making you more reactive. Protecting your primary partnership means aligning on a Unified Financial Protocol.

-

The Psychological Cost of Becoming the “Family ATM”

Over time, a lack of boundaries causes a subtle identity shift. You stop feeling like a parent and start feeling like a Financial Institution. Every phone call becomes transactional, and every text notification triggers “Request Anxiety.”

Signs of Emotional Burnout:

- You feel stressed when your phone rings.

- You justify support you’re actually uncomfortable with.

- You feel unappreciated for the “Resource Allocation” you provide.

Implementing financial boundaries with adult children allows you to regain control. When you move from reactive “Bailout Mode” to intentional leadership, your anxiety decreases and your emotional health stabilizes.

-

Estate Planning and Inheritance Distortions

Here is a “Database Error” many parents ignore: ongoing financial support now can distort inheritance later. If one child receives frequent bailouts while another remains independent, a massive imbalance forms.

The Hidden Resentment Between Siblings

Imagine Child A receives $100,000 in accumulated “help” over 15 years, while Child B receives nothing. If the final estate is split 50/50, Child B will likely feel a sense of unfairness. This is how family fractures happen.

- The Fix: Track all major transfers. Some parents choose to deduct prior “Financial Gifts” from the final inheritance to ensure the “Final Build” is fair to everyone. Transparency now prevents litigation and family “Crashes” later.

-

Cultural Expectations vs. Financial Risk

In many cultures—including India and parts of Europe—multi-generational support is a deeply held value. However, cultural value must operate within financial capacity.

The Difference Between Support and Sacrifice

Helping family is a virtue, but unlimited support that endangers your own survival is a “System Risk.”

- The Diagnostic Question: “Is this help sustainable for the next 20 years?” If the answer is no, you are sacrificing your future security for their short-term comfort. Financial boundaries with adult children allow you to balance compassion with the cold mathematics of longevity.

-

When Professional Counselling is Necessary

Sometimes, the pattern of dependency is so deep that you cannot “patch” it yourself. If financial requests are tied to emotional blackmail or chronic marital conflict, you need an external “Security Consultant.”

Financial Planners and Therapists

- Financial Planners: They can quantify the “True Cost” of your support. When the data comes from a neutral professional, the adult child’s resistance often decreases.

- Family Therapists: They can guide the communication around identity and attachment, helping you untangle the “Guilt.exe” that is overriding your logic.

The 12-Month Roadmap & Final Integration

-

The Long-Term Benefits for Your Adult Children

While implementing financial boundaries with adult children feels like a “System Restriction” in the short term, the long-term output is Competence.

- Independence Creates Growth: When the “Automatic Bailout” option returns a 403 Forbidden error, creativity appears. They begin solving problems (optimizing their code) rather than outsourcing them to you.

- Building Self-Trust: Every bill they pay independently and every financial “bug” they fix themselves builds their “Self-Trust Module.” You aren’t removing support; you are transferring responsibility, which is the ultimate goal of parenting.

-

A 12-Month Financial Boundary Implementation Roadmap

You don’t deploy a major system update all at once. You follow a structured rollout.

Month 1–2: The Audit Phase

- Action: Create your Statement of Support. Calculate every rupee/dollar that leaves your “Core Account” to support adult kids.

- Goal: Clarity on the “Resource Leak.”

Month 3–4: The Documentation Phase

- Action: Draft your Family Financial Policy. Define your “Emergency Tiers” and “No Co-signing” rules. Discuss this with your spouse to ensure “Admin Sync.”

- Goal: A written “Source of Truth.”

Month 5–6: The Communication Phase

- Action: Schedule a calm “System Sync” with your children. Explain that you are restructuring support to protect your Retirement Architecture.

- Goal: Managing expectations.

Month 7–12: The Step-Down Phase

- Action: Gradually reduce recurring support (e.g., 20% reduction per month). Move larger requests into the Structured Loan protocol.

- Goal: Achieving “Full Sandbox Mode” by the end of the year.

Expanded FAQ: Financial Boundaries with Adult Children

- Is it selfish to stop helping if I can afford it?

No. Financial boundaries with adult children are about sustainability, not scarcity. If constant support reduces their motivation to optimize their own life, you are unintentionally limiting their growth. Supporting competence is the most responsible act of love.

- What if they cut off contact because I stopped the money?

Relationships built solely on financial “pings” are fragile and unstable. If distance occurs, give the “User” time to recalibrate. When the emotional “Lag” settles, respect often replaces resentment.

- Should I ever co-sign a loan for them?

In a Phase 2.0 system, the answer is generally No. Co-signing is a “Security Vulnerability” that links your credit to their potential errors. It creates “Shared Liability” which can crash your retirement security if they default.

- How do I handle unequal support between siblings?

Transparency is the best “Patch.” Document all transfers and communicate openly. If one child needs more help now, consider adjusting the “Final Distribution” in your estate planning to keep the system fair for everyone.

- The Final Architecture: Protecting Your Legacy

Your retirement years are the culmination of decades of “System Build.” You deserve financial security, emotional peace, and predictable income. When you fail to implement financial boundaries with adult children, you risk converting your retirement into an endless cycle of “Crisis Management.”

The Core Mindset Shift (The Re-Architecture)

Move your family system from:

- Unlimited Subscriptions -> Managed Access

- Reactive Bailouts ->Structured Sandboxes

- Guilt-Based Giving -> Strategic Compassion

This is not a “Shutdown” of your love; it is a Redesign of Responsibility.

Conclusion: From Resource Leak to Wealth Architecture

In the tech world, unmanaged systems eventually fail. In your personal life, unmanaged financial support drains wealth and health. By implementing financial boundaries with adult children, you are not just saving money—you are saving your future and empowering theirs.

The Sandbox Model works because it balances compassion with structure. Love with limits. Support with sustainability. Now that the “Code” is written, it’s time to push it to production.